AI Didn’t Break Software Overnight, The Industry Factor Saw It Coming

By Diana Baechle

Senior Principal Investment Decision Research, SimCorp

The Factor Dynamics Behind the Software Industry’s Steep Decline

This week’s sell‑off did not mark the beginning of Software’s decline; the Software Industry Factor had been flashing warning signs for months, long before the market took notice.

Fears that AI advancements could threaten traditional software businesses swept through the market on Tuesday, February 2, erasing hundreds of billions of dollars in software‑related valuations. The iShares Expanded Tech‑Software Sector ETF (IGV) fell 5% on the day alone.

Yet this downturn is merely the latest chapter in a much deeper shift that has been reshaping the industry ever since the first generative AI models emerged several years ago. Early on, investors assumed AI would fuel greater software demand. But recent breakthroughs suggest AI may instead make some conventional software offerings obsolete. The launch of Anthropic’s Claude Code last month, paired with new legal‑workflow tools added to its Cowork assistant this week, highlighted how AI can sharply accelerate development cycles and compress the value of traditional software features that are rule-based, deterministic and predictable.

“The movements in the Software Industry Factor reveal that cracks had been forming beneath the surface months before the broader market recognized them.”

Many established software products risk rapid commoditization, and enterprises may increasingly prefer to build solutions in‑house rather than purchase off‑the‑shelf tools. This threat is most acute for vendors that have been slow to leverage AI to enhance productivity or scale, or to incorporate AI into their offerings. By contrast, companies delivering highly complex systems or operating in heavily regulated domains remain far more insulated.

After ChatGPT’s debut in November 2022, IGV continued its rise for several consecutive quarters, gaining 141% between January 2023 and October 2025.

But sentiment shifted sharply at the end of October 2025, when investors began questioning whether traditional software could retain its strategic importance in an AI‑centric world. IGV has since tumbled 20% year‑to‑date and 30% overall from its late‑October 2025 levels.

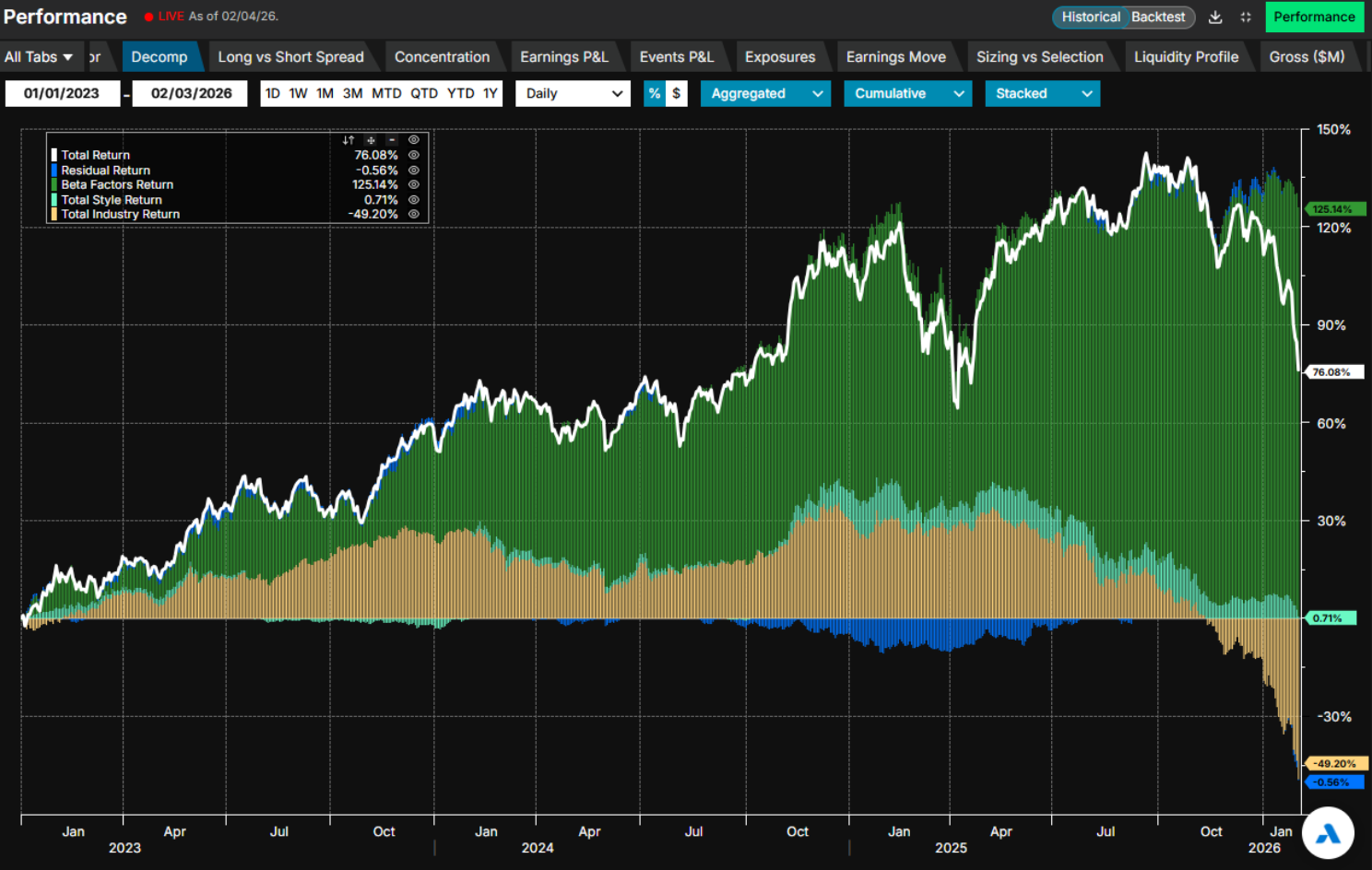

The factor‑based decomposition of IGV’s return between January 2023 and February 2026 shows that the Software Industry Factor contributed positively to the ETF’s performance for most of the period, but its contribution turned negative after the end of October 2025 and has remained negative since, according to the Axioma US5.1 Fundamental Short‑Horizon Model.

Aggregate Factor Contribution to IGV’s return 1 January 2022 – 3 February 2026

Source: Axioma, Arcana

The Software Factor's Decline

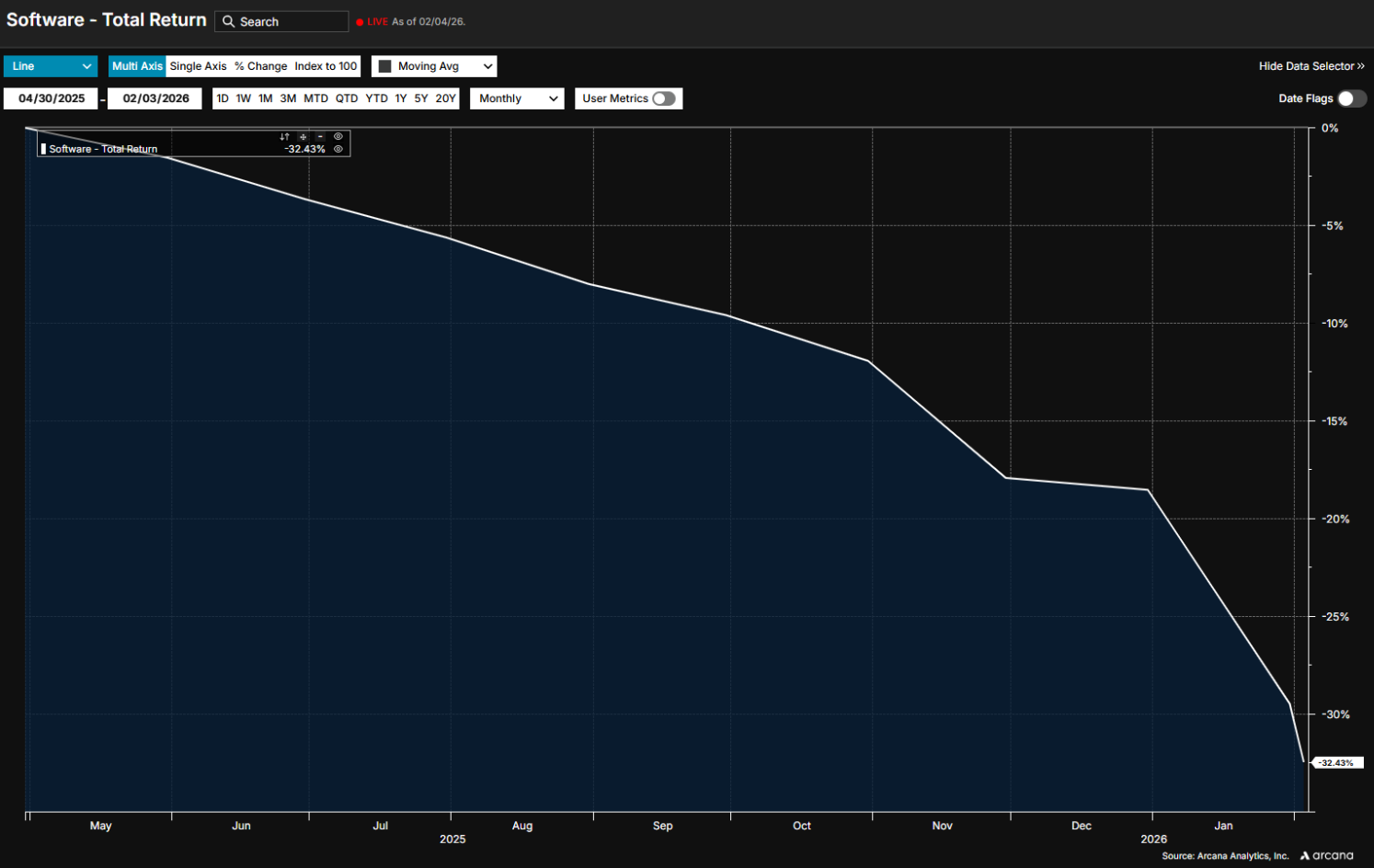

Importantly, the Software Industry Factor began declining long before IGV’s downturn in performance. Since April 2025, the factor has dropped 32%—its steepest fall in at least 35 years, based on the US5.1 Axioma model.

US51 SH Software Industry Factor – Largest drawdown in history

Source: Axioma, Arcana

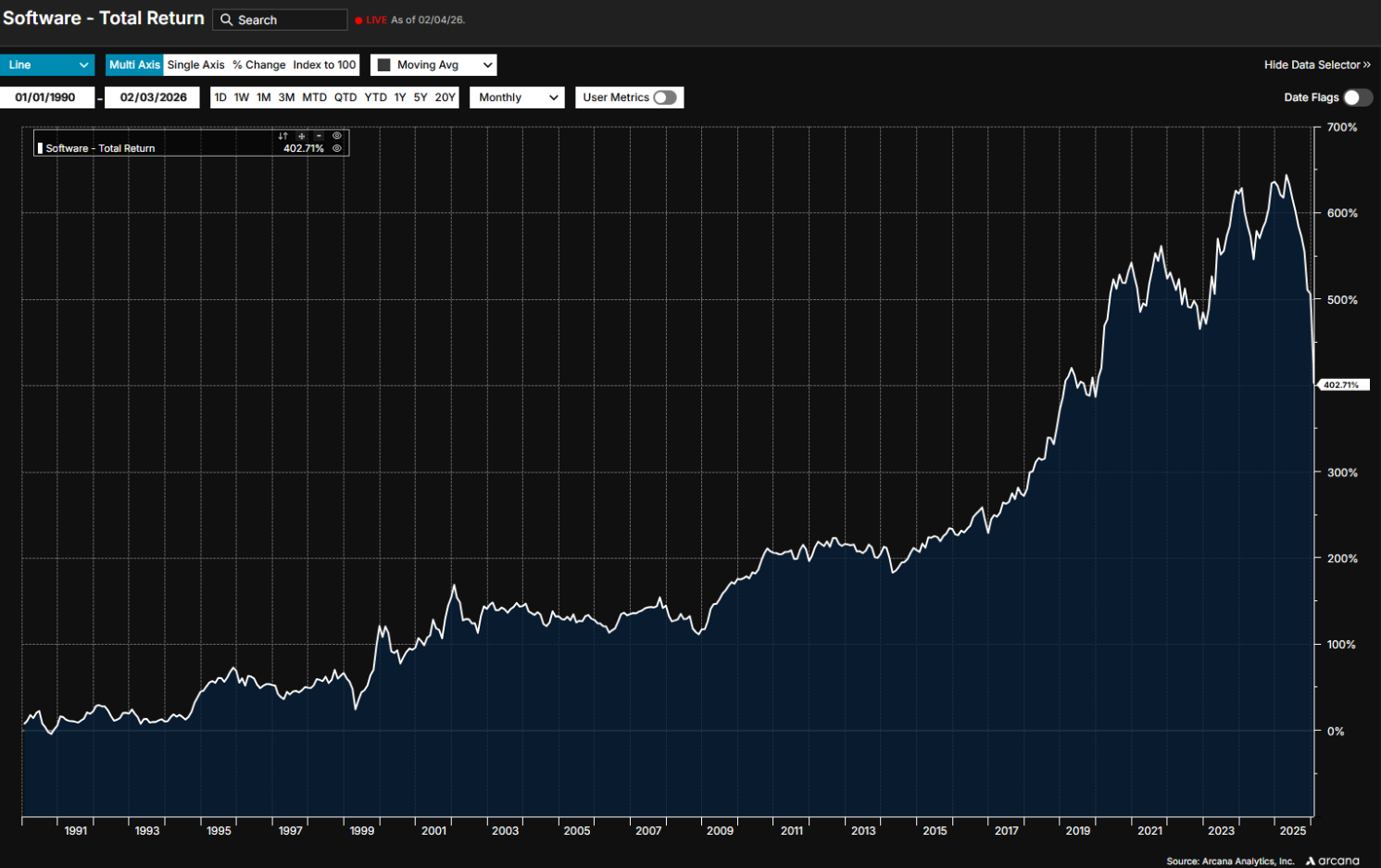

This reversal is especially striking given the Industry Factor’s decades‑long ascent, which culminated in a 35‑year high on April 30 of last year. A long list of structural tailwinds powered this rise: high‑speed internet adoption, the rapid proliferation of cloud services, subscription‑based business models, and years of ultralow interest rates that made capital abundant. The pandemic enhanced this momentum, accelerating digital transformation as nearly every sector relied more heavily on software.

Although the industry faced some resistance in 2022, spurred by rising rates and the return to office, the Software Industry Factor still posted a remarkable 170% cumulative gain over the 15 years ending April 30, 2025. That performance underscored the widespread belief that software revenue was sticky, recurring, and shielded by high switching costs.

But since April 30, 2025, that long‑standing stability has unraveled. The Software Industry Factor’s more‑than‑30% drawdown now exceeds even the losses experienced around the dot‑com bust, when the largest decline was roughly 25%. It’s also important to note that similar negative return percentages do not fully capture the magnitude of the loss because of the substantial accumulation of wealth over time. A 30% decline in the value accrued since 1990 represents a far larger absolute loss than a 25% drawdown 25 years ago, making the current downturn truly astonishing.

US51 SH Software – Historical Factor Return

Source: Axioma, Arcana

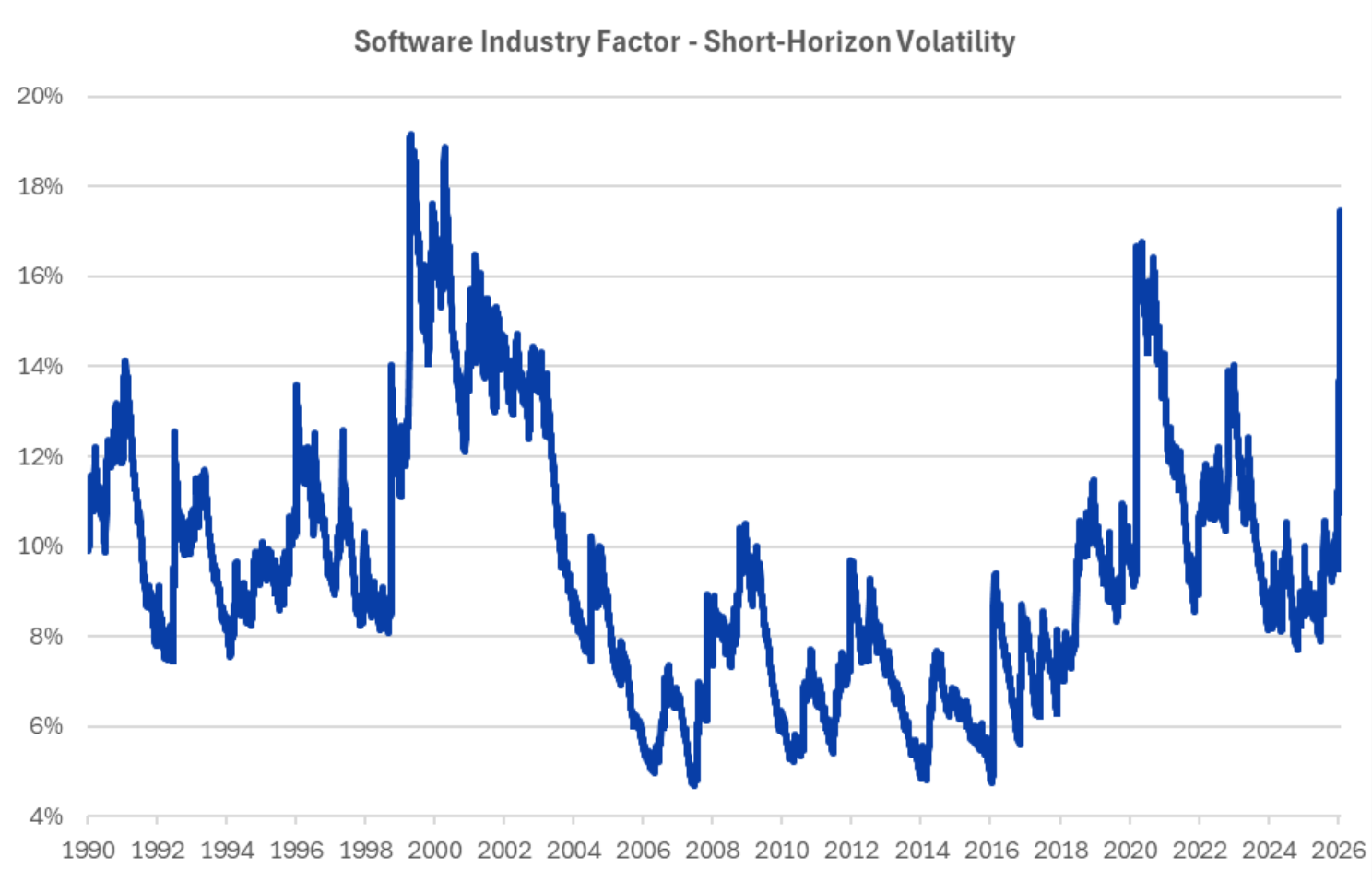

Volatility Surges to the Dot-Com Era Levels

This collapse has also been accompanied by a surge in volatility. Historically, the software industry exhibited muted swings because customers tended to remain with incumbent systems for years. Today, the Industry Factor’s volatility exceeds the peaks seen during the COVID-19 crisis and rivals the extremes recorded during the dot‑com crash, though it still remains slightly below the heights reached in 1999–2000.

US51 SH Software Industry Factor – Historical Volatility

Source: Axioma

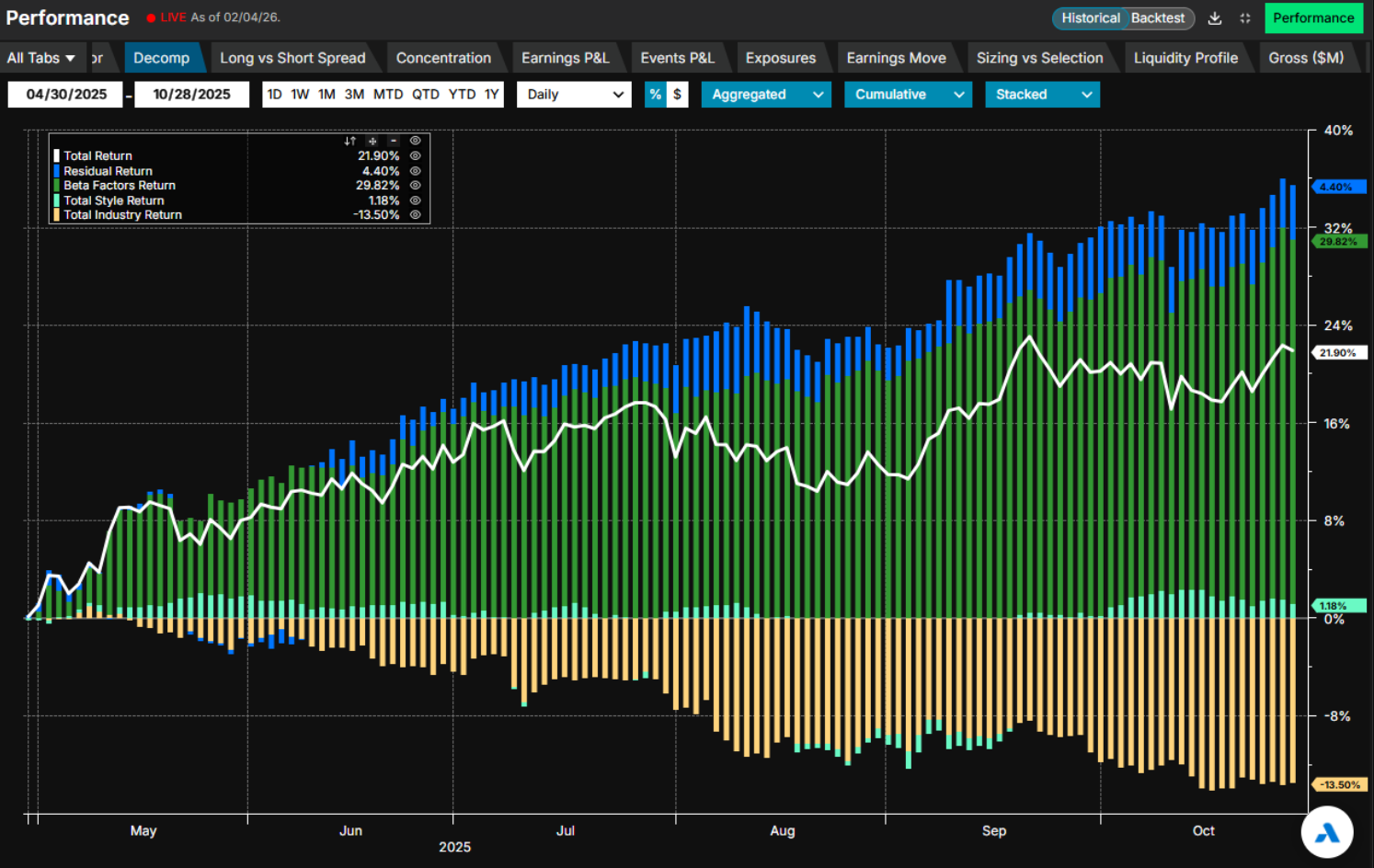

One question stands out: If the Industry Factor began deteriorating in April, why did IGV deliver strong gains between late April and late October? The answer lies entirely in market beta.

IGV’s 21.9% return during that period was driven by broad market appreciation and the high beta of its largest constituents (captured by the “Beta Factors” on the Arcana platform) which together contributed 29.8% to the ETF’s return, more than offsetting the Industry Factor’s −13.5% drag.

The aggregate Style Factor and Residual effects provided small additional boosts.

IGV Return Decomposition: 30 April 2025 – 28 October 2025

Source: Axioma, Arcana

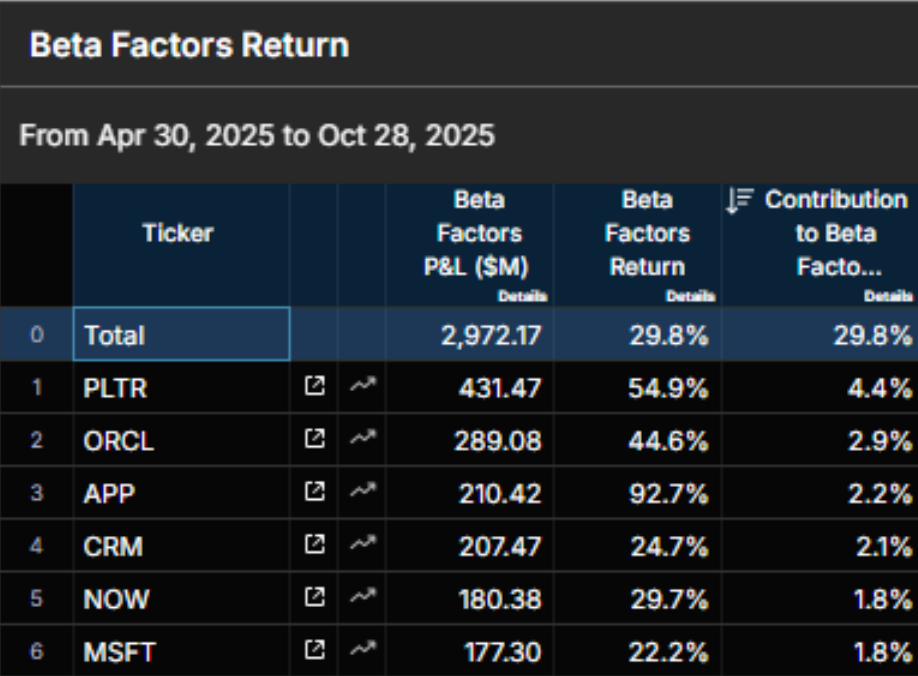

A handful of major players including Palantir (PLTR), Oracle (ORCL), AppLovin (APP), Salesforce (CRM), ServiceNow (NOW), and Microsoft (MSFT)carried the day, accounting for more than half of the Beta Factor’s 29.82% contribution.

Stock Contribution to Beta Factor Return

Source: Axioma, Arcana

What This Means for Investors

An industry once considered the unshakable darling of Wall Street has lost some of its shine. This highlights how quickly technological leadership can shift. Not long ago, software, not AI, commanded the bulk of investor enthusiasm. But the movements in the Software Industry Factor reveal that cracks had been forming beneath the surface months before the broader market recognized them. Still, leadership in technology is rarely static. As innovation continues at a rapid pace, capital could just as quickly rotate back into the Software industry—particularly if major disruptors such as Anthropic or OpenAI eventually become publicly traded companies and enter the markets under a ‘Software’ classification.

For investors, the message is clear: closely monitoring factor exposures is essential for anticipating market shifts and navigating periods of heightened volatility.

You may also be interested in